Short run costs

Now that we’ve covered some basics, let’s see what will happen to a firm’s costs in the short run.

Generally speaking, a firm’s costs of production will depend on the factors of production it uses. The relationship between the factors of production and their costs depends on two elements:

In the short run, some factors of production are fixed in the sense that they do not vary with output. These are fixed costs (Sloman, Wride, and Garratt pg 138-143). For example, rent on a property.

The total cost of using variable factors, however, does change depending on output. These are variable costs (Sloman, Wride, and Garratt pg 138-143). For example, the cost of raw materials is a variable cost.

Total Costs

The total cost (TC) of production is the sum of the total variable costs (TVC) and the total fixed costs (TFC) of production. Total fixed costs are total costs incurred by the firm for fixed inputs. Since the amount of the inputs is fixed, the total fixed costs will be the same regardless of the firm’s output rate. Total variable costs are the total costs incurred by the firm for variable inputs. The total variable cost rises as a firm’s output rises.

Thus, a simple formula to remember is:

TC = TVC + TFC

Average Costs

Average total cost (ATC, or just average cost - abbreviated AC) is the cost per unit of production. It is your total cost at certain point divided by given quantity of output:

ATC = TC/Q

As you might have guessed, average total costs can be divided into two components: fixed and variable. In other words, average total cost equals average fixed cost:

AFC = TFC/Q

Plus average variable cost:

AVC = TVC/Q

And, as a result:

ATC = AFC + AVC

Why should we care? Well, average costs affect the supply curve and are a fundamental component of supply and demand.

Marginal Cost

Marginal cost (MC) is the rise in total cost per one unit rise in output:

MC = ∆TC / ∆Q

In our example, marginal cost shows you what costs you will incur if you decide to produce one additional car. You might think that higher sales volume is better. It can be beneficial, but a good economist will tell you that sometimes it is actually better to produce (and sell) less.

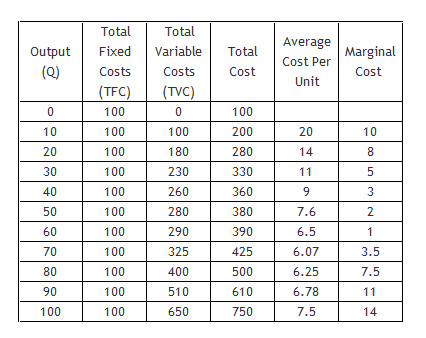

To illustrate this, let’s look at an example. The table below shows the output level (number of cars) and the costs associated with a certain output.

Generally speaking, a firm’s costs of production will depend on the factors of production it uses. The relationship between the factors of production and their costs depends on two elements:

- The productivity of the factors: Greater productivity means a smaller quantity of materials is required to produce a given level of output. Hence, the cost of that output will be lower.

- The price of the factors: The higher the price, the higher the cost of production (Sloman, Wride, and Garratt, p 138-143).

In the short run, some factors of production are fixed in the sense that they do not vary with output. These are fixed costs (Sloman, Wride, and Garratt pg 138-143). For example, rent on a property.

The total cost of using variable factors, however, does change depending on output. These are variable costs (Sloman, Wride, and Garratt pg 138-143). For example, the cost of raw materials is a variable cost.

Total Costs

The total cost (TC) of production is the sum of the total variable costs (TVC) and the total fixed costs (TFC) of production. Total fixed costs are total costs incurred by the firm for fixed inputs. Since the amount of the inputs is fixed, the total fixed costs will be the same regardless of the firm’s output rate. Total variable costs are the total costs incurred by the firm for variable inputs. The total variable cost rises as a firm’s output rises.

Thus, a simple formula to remember is:

TC = TVC + TFC

Average Costs

Average total cost (ATC, or just average cost - abbreviated AC) is the cost per unit of production. It is your total cost at certain point divided by given quantity of output:

ATC = TC/Q

As you might have guessed, average total costs can be divided into two components: fixed and variable. In other words, average total cost equals average fixed cost:

AFC = TFC/Q

Plus average variable cost:

AVC = TVC/Q

And, as a result:

ATC = AFC + AVC

Why should we care? Well, average costs affect the supply curve and are a fundamental component of supply and demand.

Marginal Cost

Marginal cost (MC) is the rise in total cost per one unit rise in output:

MC = ∆TC / ∆Q

In our example, marginal cost shows you what costs you will incur if you decide to produce one additional car. You might think that higher sales volume is better. It can be beneficial, but a good economist will tell you that sometimes it is actually better to produce (and sell) less.

To illustrate this, let’s look at an example. The table below shows the output level (number of cars) and the costs associated with a certain output.

Output of Cars and the Related Costs

Take a minute to go through the chart using the formulas we have provided. Understanding these numbers and applying the formulas from above will strengthen your understanding of the relationship between these concepts. (You can also open an excel file HERE and play with numbers, as well).

Graph of Costs

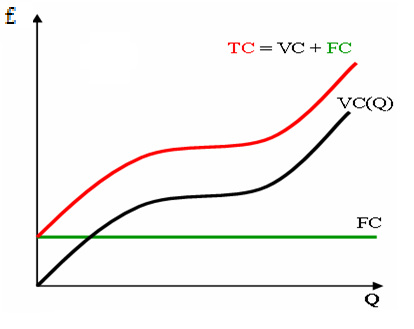

The following graph illustrates the relationship between the three cost functions:

Graph of Costs

The following graph illustrates the relationship between the three cost functions:

Cost Curves Graph 1

You might have noticed that the difference between red line (TC) and black line (VC) is equal to the intercept of the green line (FC). In other words, if we would have no fixed costs our graph would consist of only one line (TC and VC would be equal).

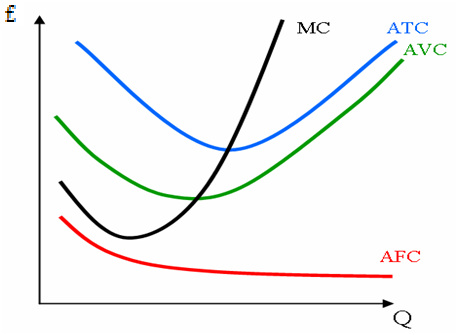

Now, let’s take it up a notch. The graph below is more complicated and includes MC, ATC, AVC, and AFC.

Now, let’s take it up a notch. The graph below is more complicated and includes MC, ATC, AVC, and AFC.

Cost Curves Graph 2

The shape of the marginal cost curve follows directly from the law of diminishing returns. Imagine you begin your car manufacturing business with just one worker. As you add more workers, overall productivity will increase. But, at certain point, there will be too many workers and each additional worker will actually make output per labourer fall. Because it gets crowded, each additional worker brings less additional output compared to addition of previous workers. That is your diminishing return.

Now let’s relate it to marginal cost. As previously stated, with each additional worker you gain more output. In other words, the change in quantity produced is larger than the change in the costs. The slope of the line for MC reflects this change by decreasing (being negative). But, starting from the point when each additional worker brings less output than a previously added worker, (read as 'change in output is less than the change in costs') the MC slope starts to increase. That’s it folks!

The average fixed costs (AFC) falls as output increases as more output is produced from the same fixed costs.

The average variable cost (AVC) curve initially falls, as the output per worker rises. Beyond a certain quantity of output, the variable costs increase as the output per worker falls.

The average total cost (ATC) is the sum of average fixed cost and average variable cost.

If you want some great additional information (or, if you understood all this, it could be a way to help you fall asleep with dreams of cost theory), please watch these YouTube videos.

Now let’s relate it to marginal cost. As previously stated, with each additional worker you gain more output. In other words, the change in quantity produced is larger than the change in the costs. The slope of the line for MC reflects this change by decreasing (being negative). But, starting from the point when each additional worker brings less output than a previously added worker, (read as 'change in output is less than the change in costs') the MC slope starts to increase. That’s it folks!

The average fixed costs (AFC) falls as output increases as more output is produced from the same fixed costs.

The average variable cost (AVC) curve initially falls, as the output per worker rises. Beyond a certain quantity of output, the variable costs increase as the output per worker falls.

The average total cost (ATC) is the sum of average fixed cost and average variable cost.

If you want some great additional information (or, if you understood all this, it could be a way to help you fall asleep with dreams of cost theory), please watch these YouTube videos.

|

|

|

Works Cited For this Page

Sloman, Wride, Garratt (2012). Economics. 8th ed. England: Pearson Education Limited. p138 – 143